Travel prices are soaring

How do consumers respond with their wallets?

A perfect storm is looming on the forecast of the airline industry. Surging oil prices tied to the war in Iran have pushed jet fuel costs up 68%, adding more than $400 million in expenses for companies in March alone.

Much of this burden is being passed on to consumers: short-term domestic ticket prices have doubled, advance fares have risen as much as 57%, and major carriers like United have trimmed routes by up to 5%. At the same time, a partial Department of Homeland Security shutdown has stretched pre-departure processing times into hours. By most measures, these conditions should be slowing traffic at the terminal.

Arrivalist’s data tell a more nuanced story. In the short term, demand appears resilient, with daily TSA arrivals and overall travel spending on the rise. Yet the number of daily travel credit card users is declining, pointing to something more troubling about the U.S. economy—growth is increasingly being driven by fewer people spending more.

Our data suggests that the closure of the Strait of Hormuz has only intensified this dynamic, amplifying already increasing spending rather than simply raising travel costs. In other words, spending isn’t rising because more people are traveling, it’s climbing because costs are inflating for those who can afford to pay the difference. Consumption is outpacing the growth of the consumer base itself. If this pattern persists, it suggests a structural shift in the industry, with air travel once again concentrating among the wealthiest travelers.

A perfect storm is looming on the forecast of the airline industry. Surging oil prices tied to the war in Iran have pushed jet fuel costs up 68%, adding more than $400 million in expenses for companies in March alone.

Much of this burden is being passed on to consumers: short-term domestic ticket prices have doubled, advance fares have risen as much as 57%, and major carriers like United have trimmed routes by up to 5%. At the same time, a partial Department of Homeland Security shutdown has stretched pre-departure processing times into hours. By most measures, these conditions should be slowing traffic at the terminal.

Arrivalist’s data tell a more nuanced story. In the short term, demand appears resilient, with daily TSA arrivals and overall travel spending on the rise. Yet the number of daily travel credit card users is declining, pointing to something more troubling about the U.S. economy—growth is increasingly being driven by fewer people spending more.

Our data suggests that the closure of the Strait of Hormuz has only intensified this dynamic, amplifying already increasing spending rather than simply raising travel costs. In other words, spending isn’t rising because more people are traveling, it’s climbing because costs are inflating for those who can afford to pay the difference. Consumption is outpacing the growth of the consumer base itself. If this pattern persists, it suggests a structural shift in the industry, with air travel once again concentrating among the wealthiest travelers.

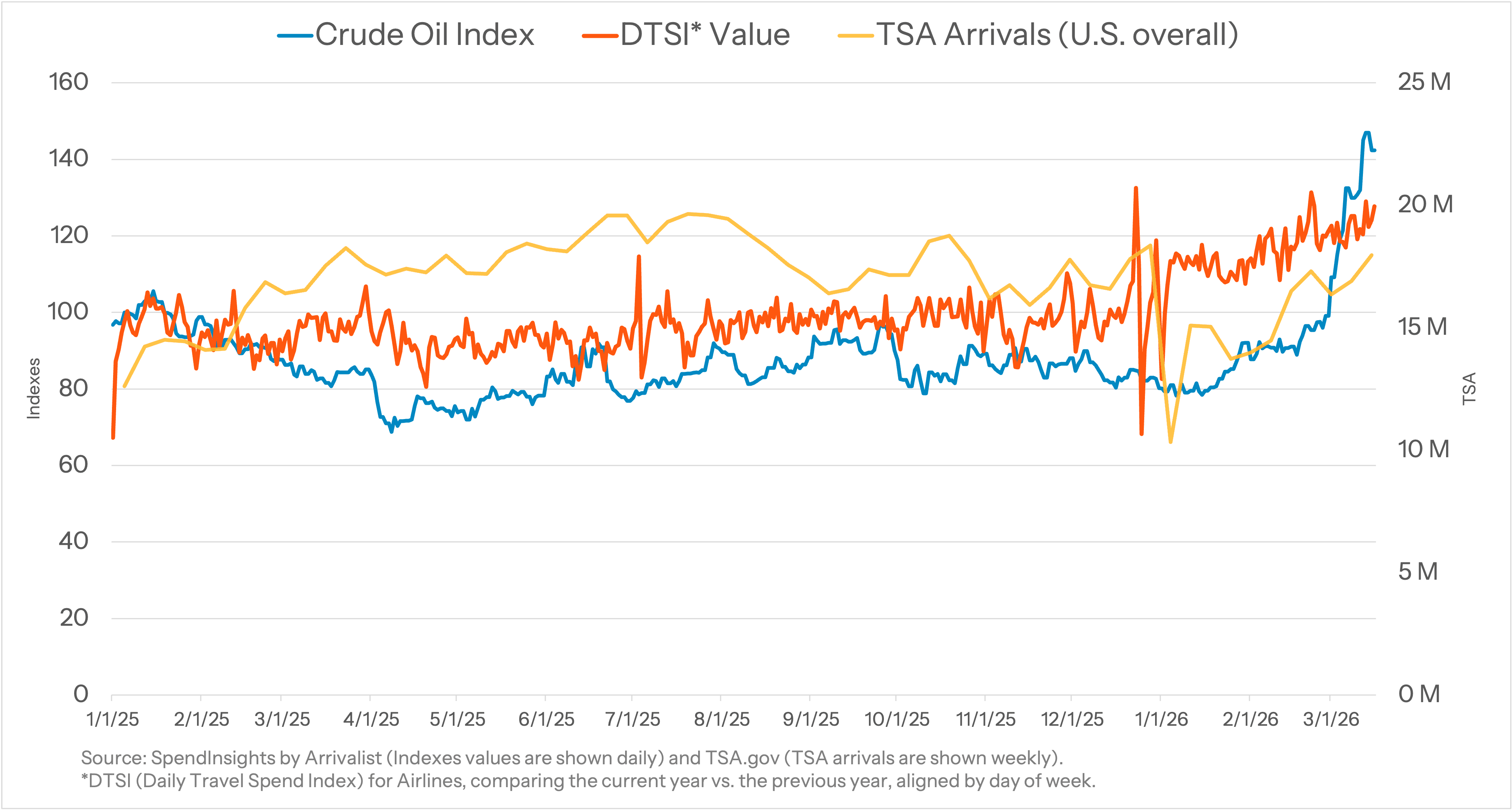

Stable Demand? Rising Spending.

Our data indicates a widening disconnect at the heart of the travel economy. Since the start of the year, daily travel spending has outpaced every underlying demand signal—TSA arrivals, travel credit card users, and even oil prices.

Comparing daily averages from Q1 2025 to Q1 2026, travel spending is up 22.40%, while travel credit card users have only grown by 17.78%, the crude oil index has risen just 6.05%, and TSA arrivals have edged up only 0.76%.

This dynamic could reflect the “K-shaped” recovery that has defined the U.S. economy since COVID-19, where growth is increasingly driven by higher-income households. Their willingness to bypass the sticker shock of surging prices for pre-departure snacks and cross-country tickets sustains top-line growth, even as lower- and middle-income consumers are steadily priced out of Summer vacations.

March Madness at the Ticketbooth

From February 28 to March 9, 2026—the first ten days of the war—daily travel spending in the United States increased by 5.33%, even as the number of daily travel credit card users fell by 3.90%. Taken together, these figures signal how the airline industry could face long-term pressure if ticket prices continue to tail rising fuel costs.

Brent crude oil opened this weekend at $113.76 per barrel, more than $40 higher than its price just before the first strikes in Iran. While the American consumer—albeit fewer in number—has absorbed higher airfares, fuel costs continue to outpace any gains from higher ticket prices. Sustaining higher fares in a shrinking market, especially when they fail to keep pace with underlying costs, does not point to stability for investors.

Additionally, during the same period, TSA arrivals increased by approximately 13% in comparison with these same days the year prior. This surge may reflect a fragile equilibrium, with more travelers choosing to fly now amid mounting geopolitical uncertainty rather than risk being priced out or grounded later.

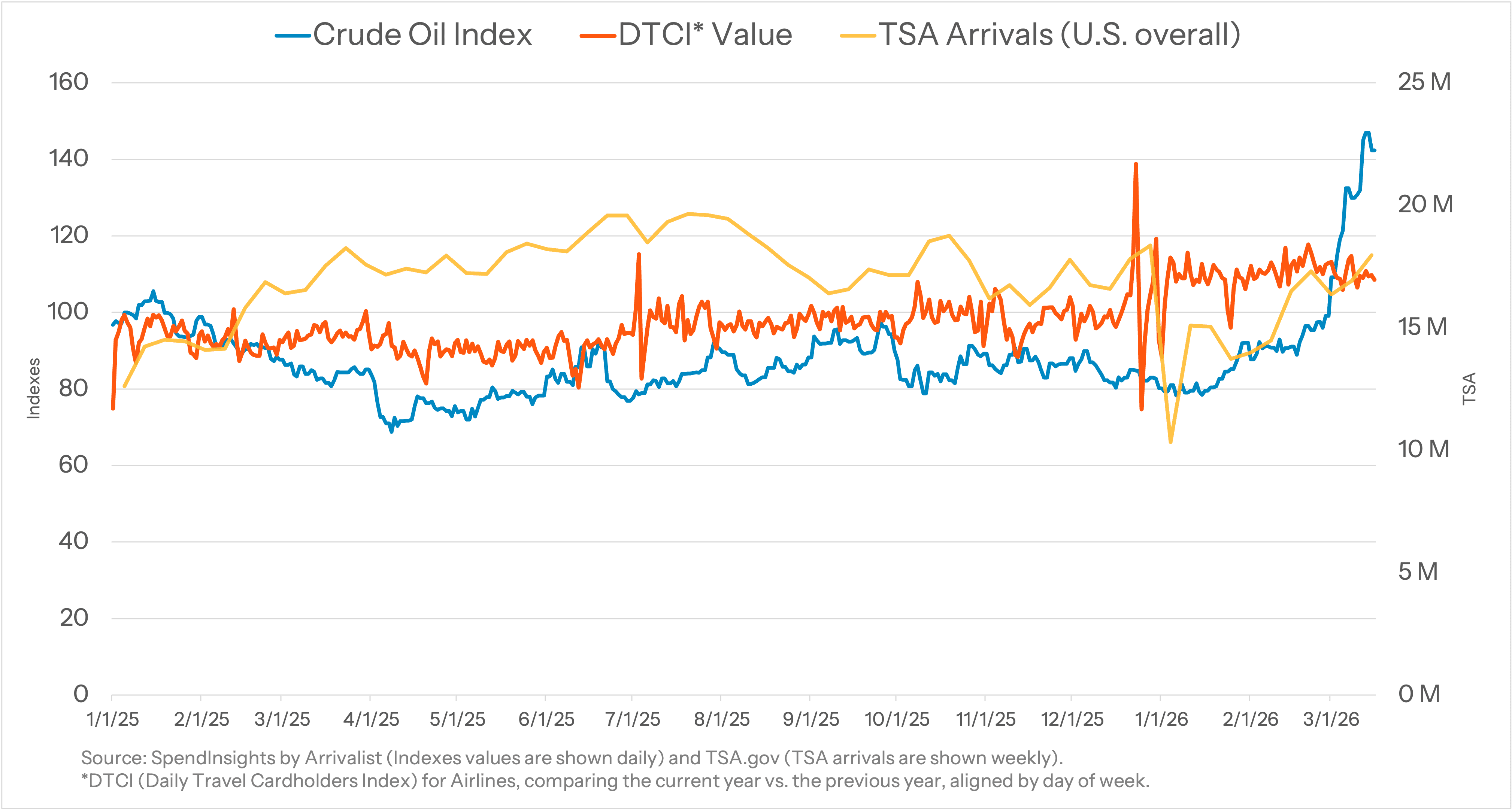

Buying Higher, Flying Later

Another factor underpinning the appearance of stability in airline spending may be weakening consumer sentiment. Rather than wait for last-minute deals, travelers appear to be locking in summer airfare now to hedge against even higher prices later. Several news outlets have echoed this urgency, encouraging flyers to book early and adjust plans down the line if needed.

Arrivalist’s data captures this frenzied-booking dynamic. On March 8, there was a sharp spike in the number of travel credit card users, aligning with United Airlines CEO Scott Kirby’s claim that it marked United Airlines’ highest-ever booking day by revenue. Ultimately, demand fell off the following day. The pattern suggests consumers may be behaving less like traditional travelers and more like commodities traders—rushing to secure tickets amid expectations that prices will keep rising.

The key question is whether demand is actually being sustained, or simply pulled forward by concerns over future affordability. If underlying indicators like daily travel credit card users continue to weaken, ticket purchases are likely to follow.

A Much Different Outlook for International Visitors

In 2025, echoing 2017, foreign arrivals to the U.S. fell by 6%, a stark contrast to rising tourism rates across the rest of the world. This drop in foreign tourism to the U.S. is projected to translate into a $8.3 billion loss in new economic activity for summer destinations that rely on peak-season travel to carry them through the year.

Over the weekend, U.S. Immigration and Customs Enforcement agents were stationed at airports to conduct heightened security screenings, including immediate arrests. With the FIFA World Cup approaching this summer—already facing backlash from astronomical ticket prices—the risk is growing that international visitors will simply stay away, redirecting their spending elsewhere and leaving U.S. cities struggling to recoup investments that can reach up to $150 million in stadiums, vendors, and security.

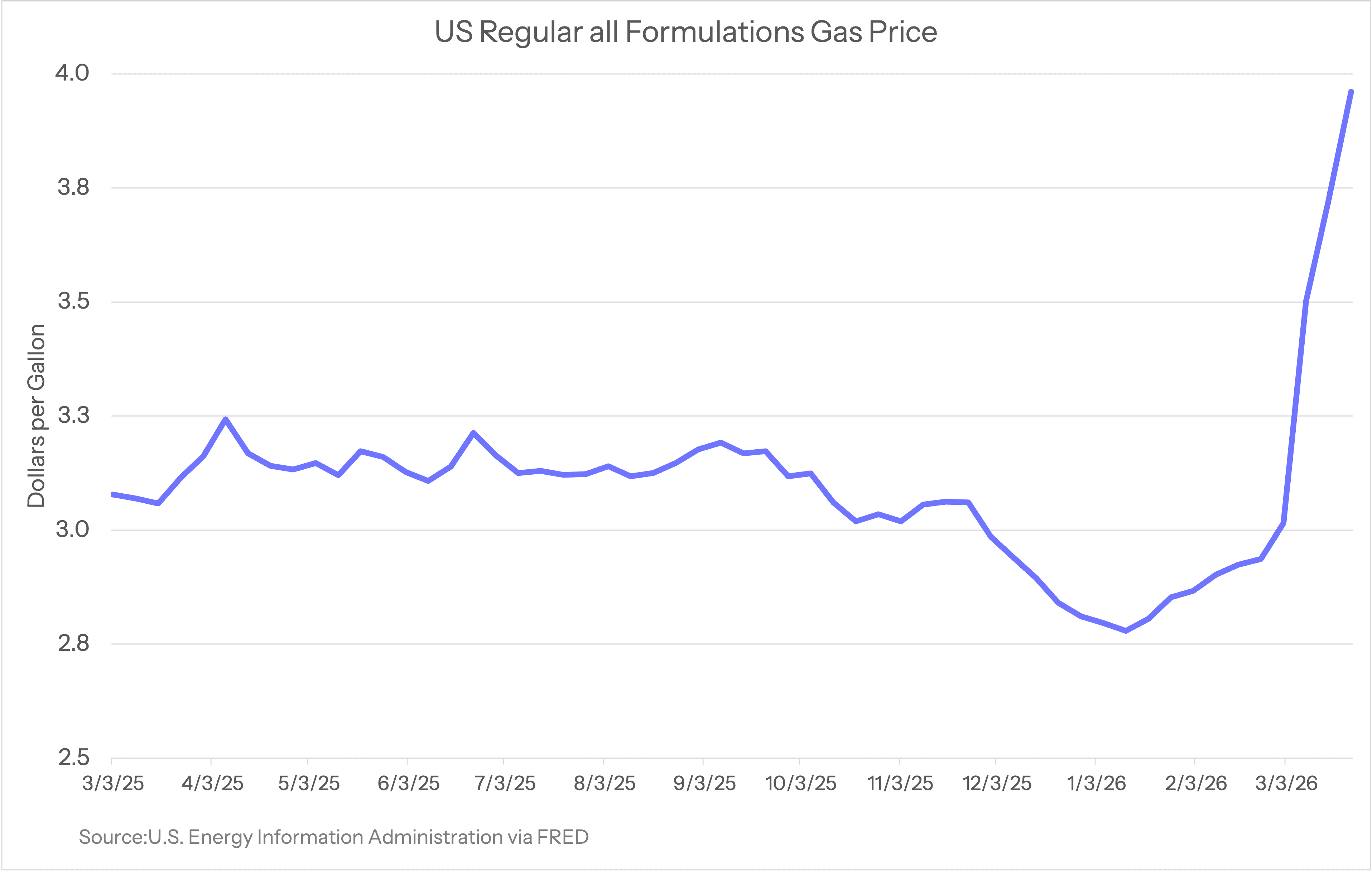

Opting for the Road Trip Instead?

The price of jet fuel is not the only energy cost on the rise. American consumers are already feeling the effects of the war in Iran at the gas pump, with average prices up nearly $1 per gallon since the beginning of March—and still climbing.

Typically, gasoline prices increase by about $0.15 per gallon in the summer as demand rises for weekend getaways, mid-distance destinations, and long-haul road trips. But gasoline has relatively inelastic demand beyond these leisure uses—people still need to commute to work, school, and daily errands. As a result, higher prices at the pump are less likely to curb fuel consumption and more likely to force households to cut back elsewhere.

This pressure is likely to intensify as crude oil costs continue to climb amid disruptions to production, processing, and shipping. These dynamics may also help explain the apparent resilience in air travel demand. As families plan summer travel, some may be opting to lock in flights now—even at elevated prices—to avoid even higher fuel costs tied to driving later.

What will Summer 2026 look like?

For airlines, the current moment threatens the stability of the entire industry. Revenue is being propped up by higher fares and a narrower base of travelers, even as underlying costs continue to climb. That imbalance raises real questions about how long this model can hold.

For travelers, this summer may mark a turning point. Those with the means to do so are locking in trips early and absorbing higher costs, while others may be getting priced out or forced to scale back.

If these trends persist, the industry risks reverting to a more exclusive model of air travel. What looks like resilience today may ultimately prove to be a temporary surge—driven not by broad demand, but by urgency, uncertainty, and increasing fuel costs.

What can DMOs do to avoid a Summer Slump in 2026?

Everyone deserves a vacation, so make sure your destination is top of mind while demand is strong.

Demonstrate why your experience is worth it:

With fewer trips in the budget this summer, every decision carries more weight. Show travelers exactly why your destination is worth their time and money—lead with what makes the experience distinctive, memorable, and impossible to replicate elsewhere.

Offer certainty in an uncertain market:

Travelers are booking earlier to hedge against rising prices—accomodate their ambition. Lean into flexible booking partnerships, “book now, adjust later” messaging, and price-lock options to reduce hesitation and capture demand before it slips away.

Remind travelers they don’t have to go far to get away:

As international and long-haul travel softens, opportunity shifts closer to home. Target short- and mid-distance audiences with messaging that emphasizes ease, accessibility, and the value of a nearby escape.

***************************************************************************************************************

DTSI (Daily Travel Spend Index) captures the total daily spend on direct airline transactions made in the US across carriers such as United, Delta, American, Southwest, Frontier, JetBlue, and others, based on a panel of credit card transactors.

DTCI (Daily Travel Cardholders Index) reflects the number of daily transactors making those direct airline purchases in the US, based on the same panel of credit card transactors.

Both are compared to the previous year, with days aligned by day of week to ensure a consistent comparison.

Stable Demand? Rising Spending.

Our data indicates a widening disconnect at the heart of the travel economy. Since the start of the year, daily travel spending has outpaced every underlying demand signal—TSA arrivals, travel credit card users, and even oil prices.

Comparing daily averages from Q1 2025 to Q1 2026, travel spending is up 22.40%, while travel credit card users have only grown by 17.78%, the crude oil index has risen just 6.05%, and TSA arrivals have edged up only 0.76%.

This dynamic could reflect the “K-shaped” recovery that has defined the U.S. economy since COVID-19, where growth is increasingly driven by higher-income households. Their willingness to bypass the sticker shock of surging prices for pre-departure snacks and cross-country tickets sustains top-line growth, even as lower- and middle-income consumers are steadily priced out of Summer vacations.

March Madness at the Ticketbooth

From February 28 to March 9, 2026—the first ten days of the war—daily travel spending in the United States increased by 5.33%, even as the number of daily travel credit card users fell by 3.90%. Taken together, these figures signal how the airline industry could face long-term pressure if ticket prices continue to tail rising fuel costs.

Brent crude oil opened this weekend at $113.76 per barrel, more than $40 higher than its price just before the first strikes in Iran. While the American consumer—albeit fewer in number—has absorbed higher airfares, fuel costs continue to outpace any gains from higher ticket prices. Sustaining higher fares in a shrinking market, especially when they fail to keep pace with underlying costs, does not point to stability for investors.

Additionally, during the same period, TSA arrivals increased by approximately 13% in comparison with these same days the year prior. This surge may reflect a fragile equilibrium, with more travelers choosing to fly now amid mounting geopolitical uncertainty rather than risk being priced out or grounded later.

Buying Higher, Flying Later

Another factor underpinning the appearance of stability in airline spending may be weakening consumer sentiment. Rather than wait for last-minute deals, travelers appear to be locking in summer airfare now to hedge against even higher prices later. Several news outlets have echoed this urgency, encouraging flyers to book early and adjust plans down the line if needed.

Arrivalist’s data captures this frenzied-booking dynamic. On March 8, there was a sharp spike in the number of travel credit card users, aligning with United Airlines CEO Scott Kirby’s claim that it marked United Airlines’ highest-ever booking day by revenue. Ultimately, demand fell off the following day. The pattern suggests consumers may be behaving less like traditional travelers and more like commodities traders—rushing to secure tickets amid expectations that prices will keep rising.

The key question is whether demand is actually being sustained, or simply pulled forward by concerns over future affordability. If underlying indicators like daily travel credit card users continue to weaken, ticket purchases are likely to follow.

A Much Different Outlook for International Visitors

In 2025, echoing 2017, foreign arrivals to the U.S. fell by 6%, a stark contrast to rising tourism rates across the rest of the world. This drop in foreign tourism to the U.S. is projected to translate into a $8.3 billion loss in new economic activity for summer destinations that rely on peak-season travel to carry them through the year.

Over the weekend, U.S. Immigration and Customs Enforcement agents were stationed at airports to conduct heightened security screenings, including immediate arrests. With the FIFA World Cup approaching this summer—already facing backlash from astronomical ticket prices—the risk is growing that international visitors will simply stay away, redirecting their spending elsewhere and leaving U.S. cities struggling to recoup investments that can reach up to $150 million in stadiums, vendors, and security.

Opting for the Road Trip Instead?

The price of jet fuel is not the only energy cost on the rise. American consumers are already feeling the effects of the war in Iran at the gas pump, with average prices up nearly $1 per gallon since the beginning of March—and still climbing.

Typically, gasoline prices increase by about $0.15 per gallon in the summer as demand rises for weekend getaways, mid-distance destinations, and long-haul road trips. But gasoline has relatively inelastic demand beyond these leisure uses—people still need to commute to work, school, and daily errands. As a result, higher prices at the pump are less likely to curb fuel consumption and more likely to force households to cut back elsewhere.

This pressure is likely to intensify as crude oil costs continue to climb amid disruptions to production, processing, and shipping. These dynamics may also help explain the apparent resilience in air travel demand. As families plan summer travel, some may be opting to lock in flights now—even at elevated prices—to avoid even higher fuel costs tied to driving later.

What will Summer 2026 look like?

For airlines, the current moment threatens the stability of the entire industry. Revenue is being propped up by higher fares and a narrower base of travelers, even as underlying costs continue to climb. That imbalance raises real questions about how long this model can hold.

For travelers, this summer may mark a turning point. Those with the means to do so are locking in trips early and absorbing higher costs, while others may be getting priced out or forced to scale back.

If these trends persist, the industry risks reverting to a more exclusive model of air travel. What looks like resilience today may ultimately prove to be a temporary surge—driven not by broad demand, but by urgency, uncertainty, and increasing fuel costs.

What can DMOs do to avoid a Summer Slump in 2026?

Everyone deserves a vacation, so make sure your destination is top of mind while demand is strong.

Demonstrate why your experience is worth it:

With fewer trips in the budget this summer, every decision carries more weight. Show travelers exactly why your destination is worth their time and money—lead with what makes the experience distinctive, memorable, and impossible to replicate elsewhere.

Offer certainty in an uncertain market:

Travelers are booking earlier to hedge against rising prices—accomodate their ambition. Lean into flexible booking partnerships, “book now, adjust later” messaging, and price-lock options to reduce hesitation and capture demand before it slips away.

Remind travelers they don’t have to go far to get away:

As international and long-haul travel softens, opportunity shifts closer to home. Target short- and mid-distance audiences with messaging that emphasizes ease, accessibility, and the value of a nearby escape.

***************************************************************************************************************

DTSI (Daily Travel Spend Index) captures the total daily spend on direct airline transactions made in the US across carriers such as United, Delta, American, Southwest, Frontier, JetBlue, and others, based on a panel of credit card transactors.

DTCI (Daily Travel Cardholders Index) reflects the number of daily transactors making those direct airline purchases in the US, based on the same panel of credit card transactors.

Both are compared to the previous year, with days aligned by day of week to ensure a consistent comparison.