Arrival at Altitude | Steamboat Spotlight

Leading up to my recent Steamboat Springs trip over the holiday break, countless neighbors walking their dogs advised me, “There’s no snow in the Rockies this year!” As if we’d change our trip. We live to travel. Their warnings seemed a bit dramatic and I assured them of our intent to enjoy the destination in full, regardless of precipitation levels. We had a wonderful trip that included lifetime milestones: my first Stetson hat from F.M. Light to complete my Western transformation, my daughter’s first convincing Blue run, our son’s first time fumbling around on ice skates (much to the amusement of spectators), and our family’s first soak in Steamboat Hot Springs. As I warmed my bones by the fire that first evening, I wondered to what extent visitor behavior and the local economy were impacted by the weather that season.

Through late 2025, the Colorado Rockies were met with challenging framework conditions, from labor issues to low snow. This called into question how skiers and visitors overall responded with their wallets. Despite the recent snowfall, many ski destinations lost economic opportunity from the sparse early season.

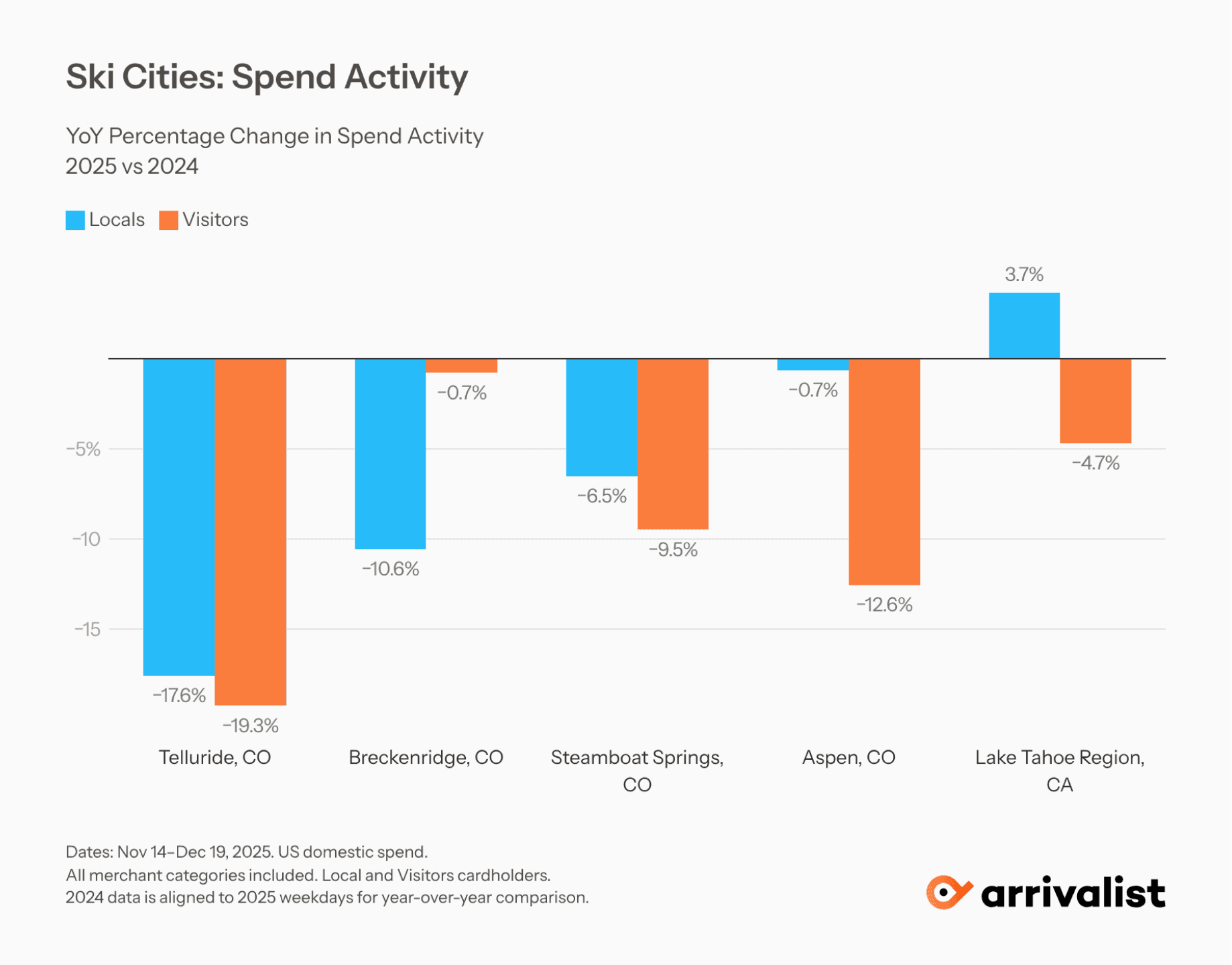

Steamboat was certainly not alone. Arrivalist examined credit card transactions at scale to sample a number of ski destinations in the competitive set. Steamboat’s total spend from visitors (those who traveled more than 50 miles to the destination) was down nearly 10%, while locals (those residing within the 50 mile radius) pulled back only 6.5% for the same time period. Contrast this to Telluride, where acute labor challenges and closure limited visitation, and to the Lake Tahoe resorts, where locals responded eagerly to fresh powder.

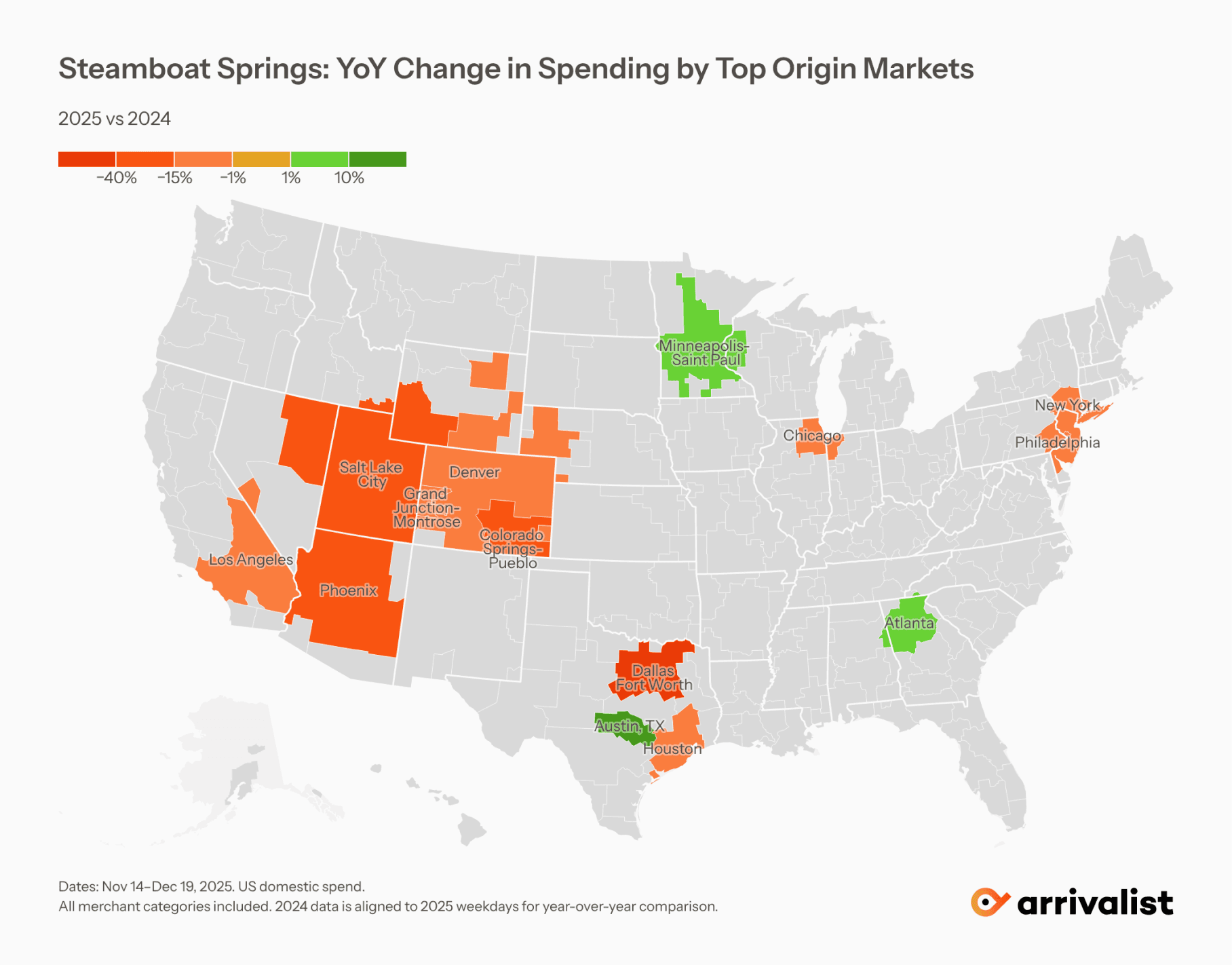

My hypothesis was that far-flung destinations with different climates and landscapes would prove less elastic to the snow level. After all, there was no stopping this inelastic family of economists from their long-awaited Colorado vacation. Among the top 15 markets for total spend, the markets with the highest concentration of world class skiing (think Mammoth for the LA DMA) pulled back hardest. Southern markets including Atlanta and Austin actually increased their spend, as did Minneapolis-St. Paul. However, the trend was not monolithic. Other Texas markets including Dallas and Houston were also down Year over Year.

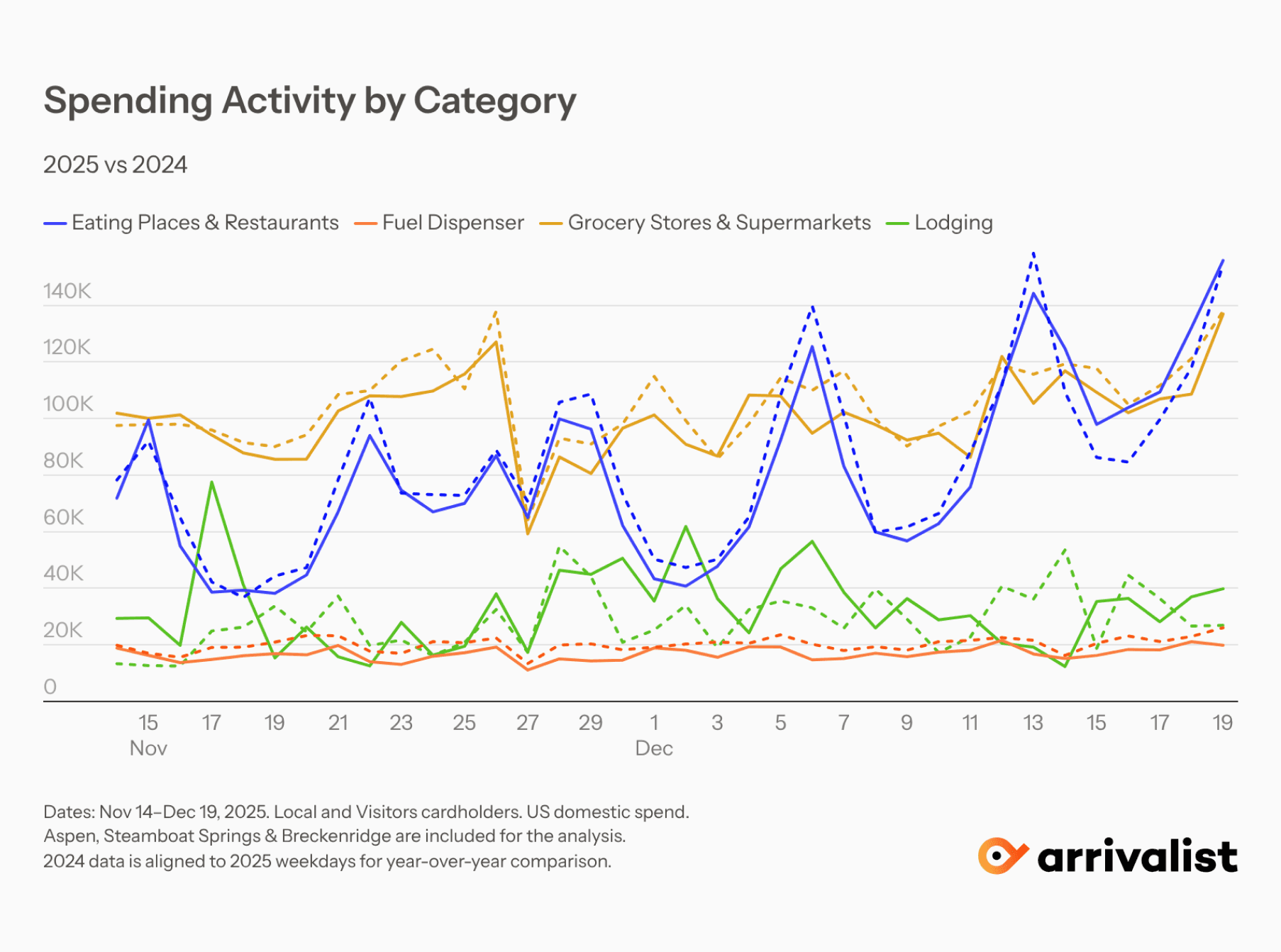

Across the top four merchant categories, spend levels also declined year over year. For a destination like Steamboat, with so many locally-owned family restaurants, even seemingly subtle drops in spending can shape an entire sector economically. Locally owned businesses have higher multiplier effects, meaning that the money tends to stay in the economy and spur spending beyond the initial transactions.

For us, fewer travelers meant we could slip into Mazzola’s cozy Italian underground without reservations and safely careen down the mountain with minimal lines awaiting us at the gondola or chair lift. For the local economy, however, balancing volume and yield impacts everything from hiring to marketing decisions, far beyond leisure.

If we step back, can we attribute these drops to the early season low-snow conditions, or labor in the case of Telluride? Are we looking at wavering consumer sentiment about the economy or the spectre of climate change?

Our larger indicators are Ikon and Epic pass sales. Both providers sell lift tickets, lodging bundles, and other amenities for mountain resorts across the world. Arrivalist observes substantial year over year declines when we aggregate the two providers’ sales. Overall, when we examine Jan 1 - Dec 19 sales (capturing a broad swathe, from the early bird promotions to late season sales), we see a 34.1% drop in cardholders and a 34.6% drop in total spend YoY. These findings suggest we are seeing a global shift rather than just a regional one.

With these considerations, how can other destinations learn from this season and prepare for similar conditions in the future?

Marketing

Target less snow-elastic markets who value the novelty of the destination as a whole– not just the world-class ski resort.

Narrow in on the high-value traveler to optimize for yield off the mountain.

Identify markets likeliest to leave a positive economic impact outside the resort (higher multiplier effect).

Lifetime value/friction reduction

Enhance in-destination spend with push alerts from Ikon/Epic on nearby activities. Rather than thinking of maximizing short-term revenues in the resort itself, promotethe lifetime value of the customer who experiences all the destination has to offer. This requires public-private cooperation in the moment.

Provide real-time suggestions on nearby restaurants with cancelations/openings/no wait/family-friendly, etc. This would reduce visitor friction.

Ensure accuracy of digital trail maps with suggestions on different ways down the mountain (visitors can't rely on physical signage alone). Weather is out of the resort's control, but digital signage certainly is under their purview.

At Arrivalist, we encourage our team to travel responsibly, contemplate their economic impact, reduce negative externalities, and observe tourism at ground (or mountaintop) level. Our vacations are our vocations. From beaches to mountains, we are connecting the dots between leisure trips and better destination outcomes in support of our mission statement: Empower destination decision-makers with data as a force for good, providing insights that enhance quality of life.

***

Arrivalist offers the tourism industry’s highest-fidelity, fastest-to-market spend data, revealing trends in seasonability, origin markets, and in-destination spend by category. Sign up here for a complimentary view of your destination’s economy, with results updated every week.

Leading up to my recent Steamboat Springs trip over the holiday break, countless neighbors walking their dogs advised me, “There’s no snow in the Rockies this year!” As if we’d change our trip. We live to travel. Their warnings seemed a bit dramatic and I assured them of our intent to enjoy the destination in full, regardless of precipitation levels. We had a wonderful trip that included lifetime milestones: my first Stetson hat from F.M. Light to complete my Western transformation, my daughter’s first convincing Blue run, our son’s first time fumbling around on ice skates (much to the amusement of spectators), and our family’s first soak in Steamboat Hot Springs. As I warmed my bones by the fire that first evening, I wondered to what extent visitor behavior and the local economy were impacted by the weather that season.

Through late 2025, the Colorado Rockies were met with challenging framework conditions, from labor issues to low snow. This called into question how skiers and visitors overall responded with their wallets. Despite the recent snowfall, many ski destinations lost economic opportunity from the sparse early season.

Steamboat was certainly not alone. Arrivalist examined credit card transactions at scale to sample a number of ski destinations in the competitive set. Steamboat’s total spend from visitors (those who traveled more than 50 miles to the destination) was down nearly 10%, while locals (those residing within the 50 mile radius) pulled back only 6.5% for the same time period. Contrast this to Telluride, where acute labor challenges and closure limited visitation, and to the Lake Tahoe resorts, where locals responded eagerly to fresh powder.

My hypothesis was that far-flung destinations with different climates and landscapes would prove less elastic to the snow level. After all, there was no stopping this inelastic family of economists from their long-awaited Colorado vacation. Among the top 15 markets for total spend, the markets with the highest concentration of world class skiing (think Mammoth for the LA DMA) pulled back hardest. Southern markets including Atlanta and Austin actually increased their spend, as did Minneapolis-St. Paul. However, the trend was not monolithic. Other Texas markets including Dallas and Houston were also down Year over Year.

Across the top four merchant categories, spend levels also declined year over year. For a destination like Steamboat, with so many locally-owned family restaurants, even seemingly subtle drops in spending can shape an entire sector economically. Locally owned businesses have higher multiplier effects, meaning that the money tends to stay in the economy and spur spending beyond the initial transactions.

For us, fewer travelers meant we could slip into Mazzola’s cozy Italian underground without reservations and safely careen down the mountain with minimal lines awaiting us at the gondola or chair lift. For the local economy, however, balancing volume and yield impacts everything from hiring to marketing decisions, far beyond leisure.

If we step back, can we attribute these drops to the early season low-snow conditions, or labor in the case of Telluride? Are we looking at wavering consumer sentiment about the economy or the spectre of climate change?

Our larger indicators are Ikon and Epic pass sales. Both providers sell lift tickets, lodging bundles, and other amenities for mountain resorts across the world. Arrivalist observes substantial year over year declines when we aggregate the two providers’ sales. Overall, when we examine Jan 1 - Dec 19 sales (capturing a broad swathe, from the early bird promotions to late season sales), we see a 34.1% drop in cardholders and a 34.6% drop in total spend YoY. These findings suggest we are seeing a global shift rather than just a regional one.

With these considerations, how can other destinations learn from this season and prepare for similar conditions in the future?

Marketing

Target less snow-elastic markets who value the novelty of the destination as a whole– not just the world-class ski resort.

Narrow in on the high-value traveler to optimize for yield off the mountain.

Identify markets likeliest to leave a positive economic impact outside the resort (higher multiplier effect).

Lifetime value/friction reduction

Enhance in-destination spend with push alerts from Ikon/Epic on nearby activities. Rather than thinking of maximizing short-term revenues in the resort itself, promotethe lifetime value of the customer who experiences all the destination has to offer. This requires public-private cooperation in the moment.

Provide real-time suggestions on nearby restaurants with cancelations/openings/no wait/family-friendly, etc. This would reduce visitor friction.

Ensure accuracy of digital trail maps with suggestions on different ways down the mountain (visitors can't rely on physical signage alone). Weather is out of the resort's control, but digital signage certainly is under their purview.

At Arrivalist, we encourage our team to travel responsibly, contemplate their economic impact, reduce negative externalities, and observe tourism at ground (or mountaintop) level. Our vacations are our vocations. From beaches to mountains, we are connecting the dots between leisure trips and better destination outcomes in support of our mission statement: Empower destination decision-makers with data as a force for good, providing insights that enhance quality of life.

***

Arrivalist offers the tourism industry’s highest-fidelity, fastest-to-market spend data, revealing trends in seasonability, origin markets, and in-destination spend by category. Sign up here for a complimentary view of your destination’s economy, with results updated every week.

Want to see how your specific destination performed against these national trends?

Contact us for a personalized insights report

Want to see how your specific destination performed against these national trends?

Contact us for a personalized insights report

Thanksgiving 2025

The “Record-Breaking” 2025 Thanksgiving travel hype missed the mark.

Knoxville 2025

Game days move more than fans

Privacy Law Changes

Changes that affect the use of location data